On October 2, 2020, the SBA issued a Procedural Notice with guidance regarding changes in ownership of an entity that has received PPP funds. The Notice defines “change of ownership” as follows:

The Notice stipulates an entity that received PPP funds remains responsible for 1) the performance of all obligations under the PPP, 2) all certifications made in connection with the PPP application, 3) compliance with all other PPP requirements, and 4) maintaining documentation and providing that documentation to the PPP lender or the SBA upon request. In the case of a merger of the PPP borrower into another entity, the successor to the PPP borrower will be subject to all obligations under the PPP loan.

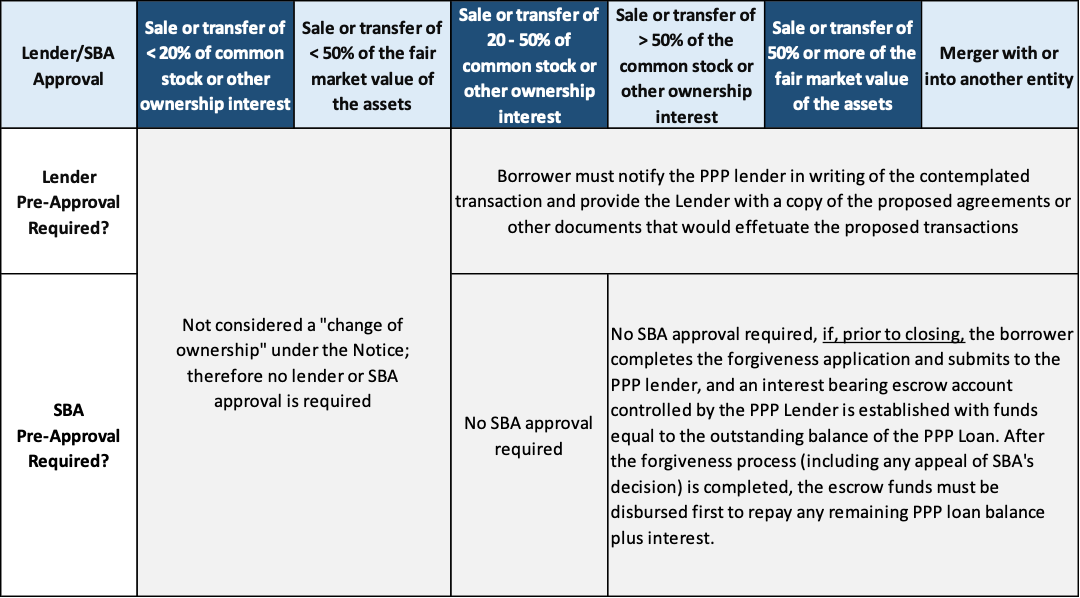

The Notice also outlines the circumstances that require the prior approval of a change in ownership of a PPP borrower by the PPP lender and the SBA.

If the PPP note has been fully satisfied, either through repayment or completion of the forgiveness process, then there are no restrictions on a change in ownership. The forgiveness process is considered complete if the SBA has remitted funds to the lender and the borrower has repaid any remaining balance due.

For cases in which the PPP note has not been fully satisfied prior to the change in ownership, the following chart summarizes the circumstances and pre-approval requirements outlined in the Notice:

The Notice also requires that all sales and other transfers occurring since the date of the approval of the PPP loan must be aggregated in determining if the relevant thresholds have been met.

More than one PPP loan following a change in ownership or merger

If a change in ownership occurs through a sale of stock or other ownership interest, the borrower and new owner must segregate their respective PPP funds and track the spending of their respective PPP funds separately. Each borrower will need to be able to demonstrate compliance with the PPP requirements separately. In the case of a merger, the successor entity must segregate and separately track the funds to ensure compliance with respect to each PPP loan.

SBA Approval

In cases of a transfer of more than 50 percent of the ownership interest or 50 percent or more of the fair market value of assets, SBA pre-approval will be required when the PPP note has not been satisfied and the requirements for the borrower to submit a forgiveness application and establish an escrow account cannot be met. The lender is responsible for obtaining approval from the SBA, and Notice provides a list of the information that must be included with the approval request.

The Notice states that SBA approval of any change of ownership involving the sale of 50 percent or more of the fair market value of the assets will require the purchasing entity to assume all of the PPP borrower’s obligations under the PPP loan. Either the purchase agreement must stipulate that the purchaser is assuming the borrower’s PPP obligations, or a separate assumption agreement may be executed and submitted to the SBA.

The SBA has 60 calendar days following the receipt of an approval request to review the information and make a determination.

Lender Responsibilities

In cases in which SBA pre-approval is not required, the Lender is required to notify the SBA within five business days following the closing of the transaction, of:

Recap of Key Takeaways

Still have questions about PPP Loan Forgiveness? Download our Frequently Asked Questions Document.

HoganTaylor has assembled a team to monitor developments in financial assistance available to businesses hurt by the COVID-19 pandemic. We have been working to understand the legislation and guidance being issued to support the various programs available to affected business so that we can provide relevant and timely advice to our clients. As information becomes available, we will continue to recommend specific actions to take to effectively access these programs.

If you need assistance in evaluating your company’s PPP loan certifications or in drafting documentation to support the evaluation and conclusions surrounding your certifications, please contact a HoganTaylor advisor at SBALoans@hogantaylor.com.

INFORMATIONAL PURPOSE ONLY. This content is for informational purposes only. This content does not constitute professional advice and should not be relied upon by you or any third party, including to operate or promote your business, secure financing or capital in any form, obtain any regulatory or governmental approvals, or otherwise be used in connection with procuring services or other benefits from any entity. Before making any decision or taking any action, you should consult with professional advisors.

{kind=link}