On March 27, 2020, President Trump signed the Coronavirus Aid, Relief and Economic Stimulus (CARES) Act. Under the CARES Act, the Small Business Administration began offering loans under the Paycheck Protection Program (PPP) to small businesses (including sole proprietorships and independent contractors), certain nonprofit organizations, veterans organizations, and Tribal business concerns. The PPP is designed to incentivize businesses to keep their employees and to not implement steep pay cuts during the coronavirus pandemic.

The PPP provides small businesses with loans to help pay payroll costs, mortgages, rent, and utilities during the COVID-19 (coronavirus) crisis. All payments of principal, interest, and fees under the loans are deferred for a period of time. The loans are forgiven for eligible payroll costs, mortgage or rent obligations, and certain utility payments.

ACCOUNTING FOR LOAN FORGIVENESS

The AICPA has issued a new Technical Question and Answer (TQA) under Section 3200, Long-Term Debt. The TQA updates Section 3200 by adding Section 3200.18, “Borrower Accounting for a Forgivable Loan Received Under the Small Business Administration Paycheck Protection Program.”

TQA 3200.18 asks the question, “How should a nongovernmental entity account for a forgivable loan received under the Small Business Administration Paycheck Protection Program (PPP)?”

The AICPA reply acknowledges “Given the unique nature of the PPP, questions have arisen relating to how a borrower under the program should account for the arrangement. Although the legal form of the PPP loan is debt, some believe that the loan is, in substance, a government grant.”

As such, the TQA clarifies that an entity may account for a PPP loan as a financial liability in accordance with Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 470, Debt, and ASC 405, Liabilities. Additionally, SEC registrants and nonpublic business entities can account for the PPP loan as a government grant by analogy to International Accounting Standard (IAS) 20, Accounting for Government Grants and Disclosure of Government Assistance, provided certain conditions are met.

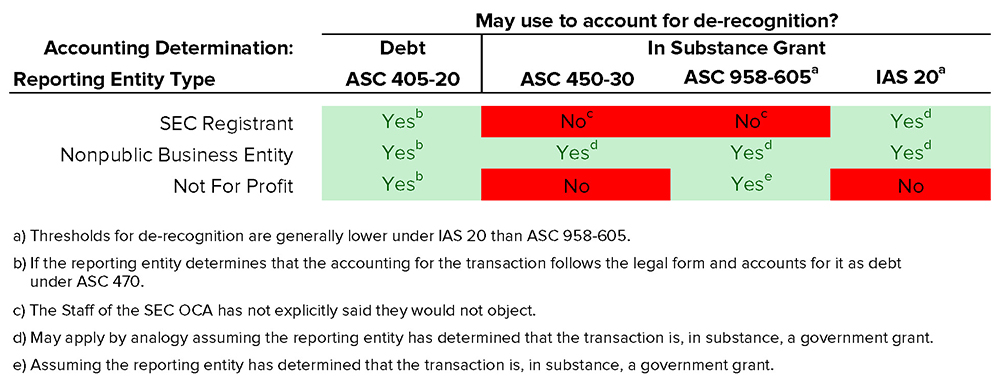

The TQA also notes other models that can be used by nonpublic business entities and Not-for-Profit (NFP) entities. For instance, nonpublic business entities and not-for-profit entities can both analogize to ASC 958, Not-for-Profit Entities, while nonpublic business entities can analogize to ASC 450, Contingencies. The table below summarizes the applicability of these accounting standards to various types of entities based on whether an entity determines the PPP loan is a financial liability (i.e debt) under ASC 470 or an in-substance grant by analogy to other accounting standards.

DEBT ACCOUNTING

If a business or NFP entity determines the PPP loan represents a financial liability under ASC 470, then an entity should accrue applicable interest in accordance with the interest method. The TQA also notes an entity is not required to impute additional interest at a market rate (even though the stated rate may be below market) because transactions representing government guaranteed obligations are exempt from rules requiring imputing interest.

Derecognition of the liability is addressed in ASC 405 which requires the proceeds from the loan remain as a liability until either (1) the debtor pays the creditor or (2) the debtor is legally released from being the primary obligor under the liability, either judicially or by the creditor. Based on this guidance, a business or NFP entity would reduce the liability and record a gain on extinguishment of debt once the entity has received a “legal release” of the loan.

IN-SUBSTANCE GRANT ACCOUNTING

NOT-FOR-PROFIT ENTITIES

The TQA states “if an NFP chooses not to follow ASC 470 and it expects to meet the PPP’s eligibility criteria and concludes that the PPP loan represents, in substance, a grant that is expected to be forgiven, it should account for such PPP loans in accordance with FASB ASC 958-605 as a conditional contribution”. A contribution is considered conditional if it has one or more barriers that must be overcome before a recipient is entitled to the assets transferred or promised. Accounting rules require that for conditional contributions, the contribution is not recognized until the conditions (or barriers) are substantially met or explicitly waived.

Therefore, NFP entities will have to assess whether the barriers created within the PPP loan forgiveness rules regarding eligible costs paid or incurred or applicable workforce requirements have been met before derecognition of the loan and recognition of income would be appropriate.

In addition to the barriers noted above, the act of submitting the loan forgiveness application and receiving the subsequent bank or SBA approval could also be considered a barrier. We anticipate NFP entities may interpret this differently. Some NFP entities will conclude that if they have clearly met the rules and regulations for loan forgiveness, the submission of the application and the subsequent approval by the bank and SBA is merely an administrative stipulation to provide a report that summarizes their performance demonstrating the underlying actions that were taken to meet the PPP loan forgiveness requirements. Other NFP entities will conclude that due to ambiguity of the rules and regulations, approval by the bank and SBA is a barrier that must be overcome before forgiveness income should be recognized.

In addition to evaluating the general requirements of the PPP program, an NFP entity would need to consider its specific facts and circumstances as to whether or not their application for forgiveness included any assumptions or interpretations of the rules and regulations that are subjective.

BUSINESS ENTITIES

The TQA states if a business entity “expects to meet the PPP’s eligibility criteria and concludes that the PPP loan represents, in substance, a grant that is expected to be forgiven, it may analogize to IAS 20 to account for the PPP loan. IAS 20 outlines a model for the accounting for different forms of government assistance, including forgivable loans. Under this model, government assistance is not recognized until there is reasonable assurance (similar to the “probable” threshold in U.S. generally accepted accounting principles that (1) any conditions attached to the assistance will be met and (2) the assistance will be received. Once there is reasonable assurance that the conditions will be met, the earnings impact of government grants is recorded “on a systematic basis over the periods in which the entity recognizes as expenses the related costs for which the grants are intended to compensate”.

Under this model, a business entity would account for the initial loan proceeds as a liability and would reduce the liability as it incurs the costs to which the loan relates. The entity would record the offset as either a credit to other income or as a reduction of the related expense. The TQA also clarifies that nonpublic business entities that conclude the PPP loan represents an in-substance grant can also analogize to ASC 958 (described previously) or to ASC 450. ASC 450 outlines the model for recognition of gain contingencies and would require all contingencies related to receipt of the PPP proceeds to have been resolved prior to recognizing the earnings impact of the loan forgiveness.

How HoganTaylor Can Help

HoganTaylor has assembled a team to monitor developments in financial assistance available to businesses hurt by the COVID-19 pandemic. We have been working to understand the legislation and guidance being issued to support the various programs available to affected business so that we can provide relevant and timely advice to our clients. As information becomes available, we will continue to recommend specific actions to take to effectively access these programs.

If you need assistance in evaluating your organization’s PPP loan accounting or in drafting documentation to support the evaluation and conclusions surrounding your certifications, please contact a HoganTaylor advisor at SBALoans@hogantaylor.com.

INFORMATIONAL PURPOSE ONLY. This content is for informational purposes only. This content does not constitute professional advice and should not be relied upon by you or any third party, including to operate or promote your business, secure financing or capital in any form, obtain any regulatory or governmental approvals, or otherwise be used in connection with procuring services or other benefits from any entity. Before making any decision or taking any action, you should consult with professional advisors.

Get Updates